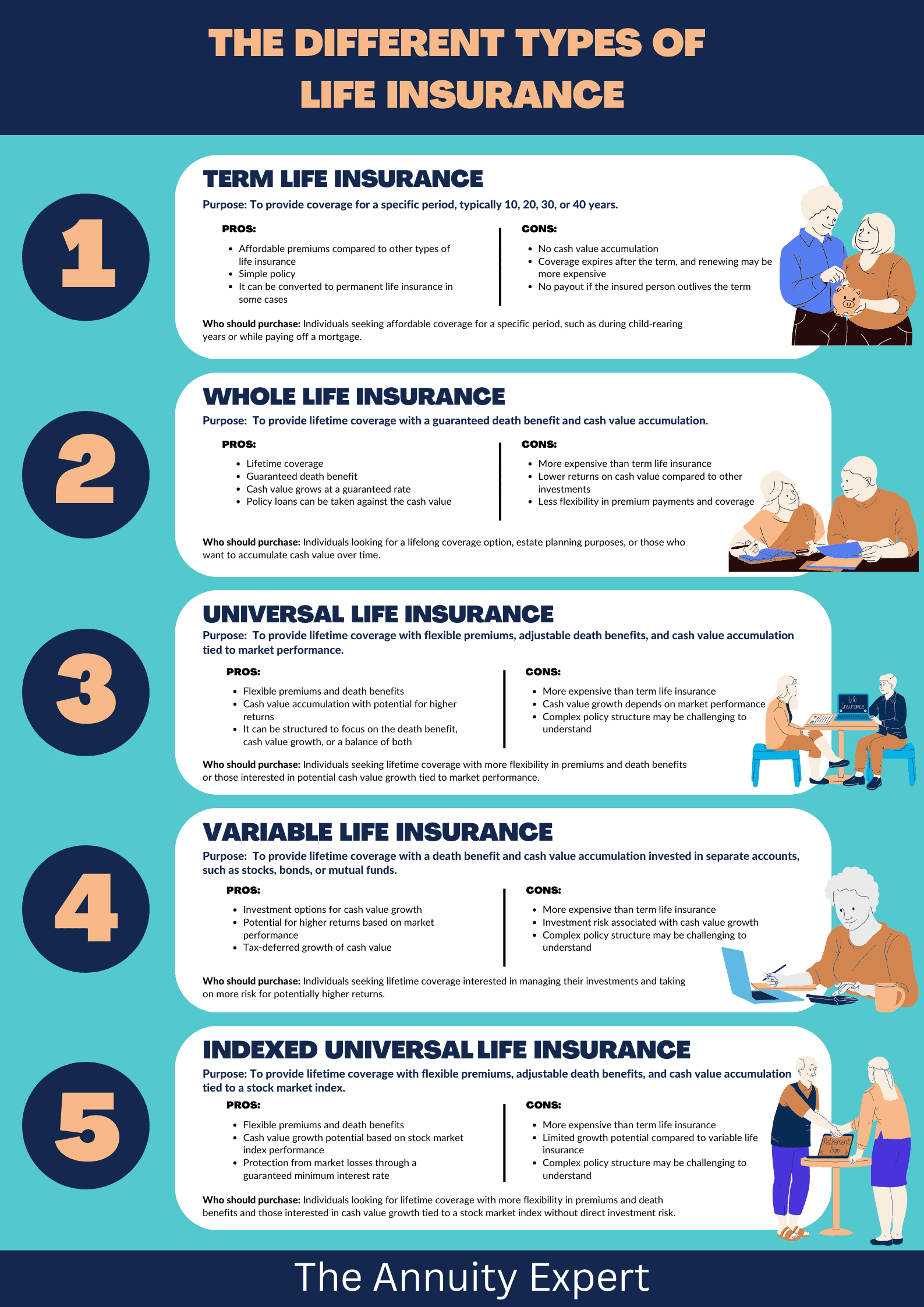

Understanding the Basics of Term Life Insurance: What You Need to Know

Term life insurance is a type of life insurance policy that provides coverage for a specific period, usually ranging from 10 to 30 years. It is designed to pay out a death benefit to your beneficiaries if you pass away during the policy's term. Without the complex cash value component found in permanent insurance plans, term life is generally more affordable and straightforward, making it an excellent option for those seeking financial protection for a limited duration. Here are some key points to understand:

- Coverage duration: Select terms that fit your financial goals.

- Affordability: Typically, lower premiums compared to whole life policies.

- Renewability: Policies may allow for renewal, often at higher rates.

When considering term life insurance, it's crucial to assess your personal circumstances and financial needs. For instance, if you have dependents or substantial debts, a term policy can provide vital protection for their financial security in the event of your untimely death. Additionally, the structured nature of these policies means you can choose a coverage amount that aligns with your obligations, such as a mortgage or children's education costs. Remember to review the policy terms, including any exclusions or potential adjustments in premiums at renewal, to ensure you make an informed choice that fits your long-term financial strategy.

How Term Life Insurance Can Provide Financial Security for Your Loved Ones

Term life insurance is a crucial financial product that can offer significant financial security for your loved ones in the event of your untimely passing. Unlike whole life insurance, term life provides coverage for a specific period, typically ranging from 10 to 30 years, allowing you to tailor your policy to the duration when your family is most dependent on your income. In the event of your death during this term, the insurance policy pays a predetermined sum to your beneficiaries, which can be used to cover daily living expenses, outstanding debts, and future needs such as education costs for your children.

Moreover, one of the most compelling features of term life insurance is its affordability. Because it typically offers no cash value component, the premiums are generally much lower than those of permanent life insurance policies. This makes it accessible for many families who wish to secure their loved ones' financial future without straining their budgets. By investing in a term life policy, you can rest easy knowing that your family will have the necessary resources to maintain their standard of living, pay off the mortgage, or handle other financial responsibilities in your absence. Thus, term life insurance stands out as a vital tool for ensuring the financial wellbeing of your loved ones.

Is Term Life Insurance the Right Choice for You? Key Factors to Consider

When contemplating whether term life insurance is the right choice for you, it is essential to assess your personal circumstances and financial goals. Term life insurance offers coverage for a specified period, typically ranging from 10 to 30 years, making it an ideal option for individuals seeking affordable premiums during critical life stages. Consider factors such as your age, health status, dependents, and any significant debts or financial obligations you may have. Understanding your needs can help you determine if a temporary coverage option meets your requirements, or if a more permanent solution like whole life insurance might be necessary.

Another crucial factor to consider is your budget and long-term financial planning. Since term life insurance tends to have lower premiums compared to whole life policies, it can free up funds for other investments or savings. However, keep in mind that once the term ends, you may need to re-evaluate your insurance options or face higher premiums due to age or health changes. Create a list of your current financial responsibilities and future plans to help clarify whether term life insurance aligns with your overall strategy. Ultimately, making an informed decision will provide you with peace of mind for both you and your loved ones.